http://rexcurry.net/moneygold.jpg

http://rexcurry.net/moneygold.jpg

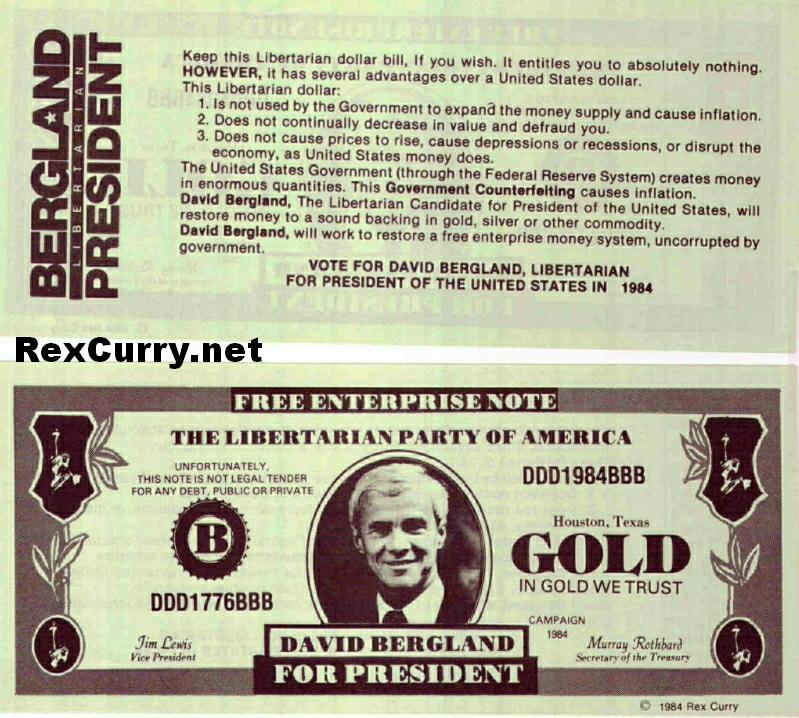

Americans were banned from buying and owning gold American coins under Roosevelt. However, Americans could enjoy more freedom (and the freedom of owning gold and American gold coins) by leaving the U.S.A.'s growing police state and traveling to Switzerland. In Switzerland, gold coins from the U.S. could be purchased in Swiss banks (though it was illegal for Americans to bring those American coins back into the U.S.). The RexCurry.net web site (that archives the work of Dr. Rex Curry, author of "Pledge of Allegiance Secrets"), received a communication from a fan who is a doctor and recalls purchasings U.S. gold coins in Switzerland in 1956. http://rexcurry.net/trip.html It is sad to note that the USA's police state did not allow private ownership of gold until 1973. The Federal Reserve Act was imposed in 1913 and it expanded the government's ability to print, counterfeit and inflate its paper money, leading to more depressions created by the government, including the Government's Depression of 1929. http://rexcurry.net/money.html These measures lessened American faith in government money. Government inspectors found that most banks were healthy, but the socialism stayed, of course. Adding insult to injury, FDR confiscated every American’s gold. That further expanded the government’s ability to counterfeit and inflate its paper money. http://rexcurry.net/moneyart.html Sure, Roosevelt paid Americans more money for the gold he seized than did Roosevelt's socialist comrade Castro. But, it is impossible to overstate the significance of Franklin Roosevelt's confiscation from Americans. The hatred of money is the root of all evil. SUPPORT CAPITALISM ! http://rexcurry.net/moneyribbon.jpg IN GOLD WE TRUST! |

| Pledge of Allegiance

in

photos and articles at http://rexcurry.net/book1a1contents-pledge.html

For fascinating information about symbolism see http://rexcurry.net/book1a1contents-swastika.html Growing Media Coverage, Radio, etc http://rexcurry.net/audio-rex-curry-podcast-radio.html Fan Mail http://rexcurry.net/pledge_heart.html |

I sincerely believe ... that banking establishments are more dangerous than standing armies, and that the principle of spending money to be paid by posterity under the name of funding is but swindling futurity on a large scale." -- Thomas Jefferson to John Taylor, 1816. "Paper is poverty,... it is only the ghost of money, and not money itself." -- Thomas Jefferson to Edward Carrington, 1788. "Scenes are now to take place as will open the eyes of credulity and of insanity itself, to the dangers of a paper medium abandoned to the discretion of avarice and of swindlers." --Thomas Jefferson to Thomas Cooper, 1814. "I now deny [the Federal Government's] power of making paper money or anything else a legal tender." -- Thomas Jefferson to John Taylor, 1798. "The maxim of buying nothing without the money in our pockets to pay for it would make of our country one of the happiest on earth." --Thomas Jefferson to Alexander Donald, 1787. "Every discouragement should be thrown in the way of men who undertake to trade without capital." --Thomas Jefferson to Nathaniel Tracy, 1785. "I am an enemy to all banks discounting bills or notes for anything but coin." --Thomas Jefferson to Thomas Cooper, 1814. "It is said that our paper is as good as silver, because we may have silver for it at the bank where it issues. This is not true. One, two, or three persons might have it; but a general application would soon exhaust their vaults, and leave a ruinous proportion of their paper in its intrinsic worthless form." --Thomas Jefferson to John W. Eppes, 1813. "Everything predicted by the enemies of banks, in the beginning, is now coming to pass. We are to be ruined now by the deluge of bank paper. It is cruel that such revolutions in private fortunes should be at the mercy of avaricious adventurers, who, instead of employing their capital, if any they have, in manufactures, commerce, and other useful pursuits, make it an instrument to burden all the interchanges of property with their swindling profits, profits which are the price of no useful industry of theirs." --Thomas Jefferson to Thomas Cooper, 1814. "We are now taught to believe that legerdemain tricks upon paper can produce as solid wealth as hard labor in the earth. It is vain for common sense to urge that nothing can produce but nothing; that it is an idle dream to believe in a philosopher's stone which is to turn everything into gold, and to redeem man from the original sentence of his Maker, 'in the sweat of his brow shall he eat his bread.'" --Thomas Jefferson to Charles Yancey, 1816. "The incorporation of a bank and the powers assumed [by legislation doing so] have not, in my opinion, been delegated to the United States by the Constitution. They are not among the powers specially enumerated." --Thomas Jefferson: Opinion on Bank, 1791. |